Florida is witnessing a significant surge in HOA and COA lien activity, with major metros seeing increases over 50%. Driven by post-Surfside legislative mandates for structural reserves, a volatile insurance market, and inflation, these liens signal growing borrower distress. Understanding Florida’s "limited super lien" framework is crucial for lenders and servicers as coastal markets face unprecedented financial pressure following recent hurricane seasons.

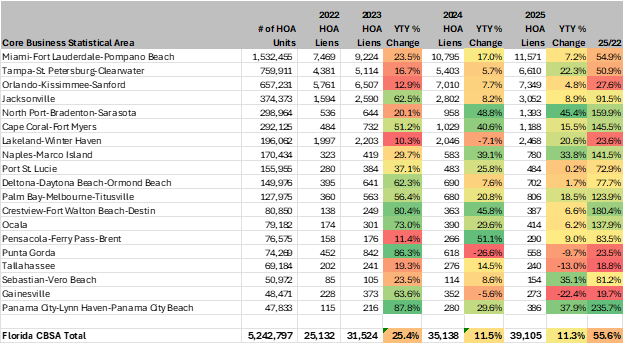

Florida’s real estate market has long been a magnet for retirees, investors, and out-of-state transplants seeking sunshine and favorable tax policies. However, alongside that growth, there is a steady uptick in Homeowner Association (HOA) and Condominium Owners Association (COA) lien activity across the state. Recent data complied by Cotality ™ in the chart above suggests the pace and geographic concentration of liens is shifting in ways that warrant closer attention.

According to recent data tracking lien volumes from 2022 to 2025, Florida is witnessing unprecedented spikes in homeowner distress. This is particularly impactful to the overall health of the housing market in Florida since 65% of listings are in HOAs, according to Realtor.com. To understand the mechanics behind the lien surge, we first have to understand Florida’s unique legal framework surrounding HOA liens. To understand the cause, we must look directly at the data , which reveals a complex story of legislative changes, insurance meltdowns, and storm-battered coastlines.

Florida’s Super Lien Status: A Different Breed

In the realm of real estate law, a "super lien" gives an HOA or COA priority over other liens on a property, including the first mortgage. In a true, absolute super lien state like Nevada or Colorado, if a homeowner defaults on their HOA dues and the association forecloses, it can theoretically wipe out the primary mortgage. This creates an existential threat for lenders, forcing them to proactively pay delinquent HOA dues to protect their collateral.

Florida, however, is not a traditional super lien state; it operates under what legal professionals refer to as a "limited super lien" or "statutory safe harbor" framework. Florida balances the financial needs of the association with the security of the mortgage lender. If a first mortgage holder forecloses on a property and takes title, their liability for the previous owner's unpaid HOA assessments is strictly capped. They are only required to pay the lesser of twelve months of past-due assessments that accrued before the lender acquired title, or one percent (1%) of the original mortgage debt. This "Safe Harbor" provision is the defining difference between Florida and true super lien states. It ensures that associations can recover some vital operating funds—preventing the financial ruin of the community—while assuring lenders that they will not face uncapped HOA debt.

Analyzing the Data: The Unprecedented Surge

Across major Florida metros, lien volumes are trending upward in a way that reflects sustained pressure rather than short-term disruption. In the massive Miami-Fort Lauderdale-Pompano Beach area—which houses more than 1.5 million HOA properties—liens have surged from 7,469 in 2022 to a projected 11,571 in 2025, a 55% increase. Tampa-St. Petersburg-Clearwater echoes this distress, jumping from 4,381 liens to 6,610 over the same period, representing a 51% increase. Even traditionally stable inland markets like Orlando-Kissimmee-Sanford have climbed to more than 7,300 liens, a 28% increase from 2022. Lien activity is rising across both large, high-density metros and smaller regional markets, suggesting that the underlying drivers are systemic rather than localized.

What is Driving the Lien Increase in Florida?

Three factors contributing to this trend are not unfamiliar to lenders and servicers. What has changed, though, is the degree to which they are converging at the same time.

- Post- Surfside Legislative Shock: Following the tragic collapse of the Champlain Towers South in Surfside in 2021, Florida passed sweeping legislation requiring associations to fully fund structural reserves, accelerating the need to address deferred maintenance. For many communities, that has translated into significant special assessments that were previously postponed. Homeowners who cannot afford sudden bills of $20,000, $50,000, or even $100,000 are falling into delinquency, which is triggering liens.

- The Insurance Meltdown: At the same time, rising insurance costs—particularly for coastal properties—have introduced additional volatility into HOA budgets. As master policy premiums increase, those costs are passed through to homeowners, often in the form of higher dues or supplemental assessments. In storm-impacted regions, these dynamics can be further amplified, and recent data underscores just how concentrated that impact has become. Some of the highest growth rates in HOA lien activity between 2022-2025 are occurring in coastal CBSAs including:

- Panama City-Lynn Haven-Panama City Beach: +236%

- Crestview-Fort Walton Beach-Destin: +180%

- North Port-Bradenton-Sarasota: +160%

- Cape Coral-Fort Myers: +145

- Naples-Marco Island: +141%

- These markets share a common thread: significant exposure to recent hurricane activity, including Ian in 2022 and Helene and Milton in 2024. In these areas, the financial ripple effects tend to follow a consistent pattern—property damage leads to insurance claims that may not fully recover rebuilding costs, leaving associations to address funding gaps through special assessments.

- Inflation: Maintenance, landscaping, pool care, and property management services have all seen sharp price increases due to general inflation and labor shortages. HOAs have no choice but to raise budgets, stretching the fixed incomes of Florida's large retiree population to the breaking point.

Individually, none of these factors are new. Together, they are creating a more compressed affordability environment that is beginning to surface more clearly in lien data.

Implications for Servicing Strategy

HOA lien activity can act as an early indicator of borrower stress, particularly in cases where rising dues or special assessments strain household budgets before mortgage delinquency occurs. As a result, visibility into these obligations becomes increasingly important in understanding borrower health holistically. Portfolios with higher concentrations in coastal or storm-impacted markets may require more targeted monitoring and borrower engagement strategies. The ability to anticipate where pressure will emerge—and respond proactively—will continue to differentiate servicing strategies.