Profitability in the mortgage market depends on surgical precision, not volume. This article explores how lenders can move beyond "spray and pray" marketing for HELOCs by targeting the intersection of low-risk collateral and high borrower propensity. By leveraging tools like Araya™ and Propensity Intelligence, lenders can prune high-risk leads and focus on the top 5% of borrowers who are 3.57x more likely to convert, turning a portfolio into a high-efficiency revenue engine.

"It's just as important to realize who NOT to contact as it is who to contact. Who not to contact avoids a complete waste of time, energy, compliance costs, and other expenses."

— COO, Major National Lender

In the current mortgage landscape, the race to grow Home Equity Line of Credit (HELOC) revenue is often run with a "spray and pray" marketing mindset. However, for the modern lender, profitability isn’t just about finding the next borrower—it’s about the surgical removal of "noise" from your solicitation list.

The strategic point of view: appetite vs. asset

Lenders must identify at scale which borrowers have the appetite for new lending products and represent low-risk opportunities. Identifying a borrower who wants a HELOC but has a property riddled with tax liens is a waste of resources. Conversely, identifying a low-risk borrower with zero propensity to borrow is an exercise in futility. Success requires the intersection of both.

The economics of marketing waste

Every "bad" lead in a HELOC campaign carries a hidden tax on your bottom line. Marketing to an unqualified or uninterested lead isn't just the cost of a stamp; it includes:

- Direct marketing costs: Creative, printing, and digital ad spend.

- Operational drag: Time spent by loan officers and processors on applications destined for denial.

- Compliance & opportunity costs: Expense of legal disclosures and the "cost" of ignoring a truly viable lead while chasing a dead end.

The Profitability Math: A campaign targeting the top 5% of a population can be 3.57 times more likely to reach a successful HELOC borrower than a random selection. By narrowing the funnel, you shift spend from "population coverage" to "conversion optimization."

A 5-Step marketing strategy

Using Cotality’s™ integrated suite of data and analytics, lenders can transform their existing customer base into a high-efficiency revenue engine. Scrub your portfolio and then use propensity models to see where your outreach will have the most impact in your book of business.

1. Market insulation: Leverage HPI

Begin by using the Cotality House Price Index (HPI) and geographical trends. Prune your database by stripping out zip codes where property values are declining. This ensures you are only targeting areas where the underlying collateral is strengthening, reducing future "underwater" risk.

2. Risk pruning: Portfolio Intelligence and Monitoring (PIM) in Araya™

Before looking for opportunity, eliminate the "blemishes." Use PIM to automatically identify and remove properties with:

- Ownership Conflicts: Properties with vesting issues or ownership transfers.

- Special Liens: Involuntary liabilities like HOA liens (which can become "Super Liens"), tax liens, or municipal judgments.

- Distress Indicators: Active pre-foreclosure or foreclosure activity.

- Negative Equity: Use the Total Home Value (THVx) AVM to calculate the current equity position from three different vantage points (Senior Liens, Your Lien + Seniors, or All Liens).

3. The "low risk" population

At this stage, you are left with a "Low Risk" list: properties in appreciating zip codes, with clear titles and healthy equity buffers.

4. Intent Identification: Propensity Intelligence in Araya

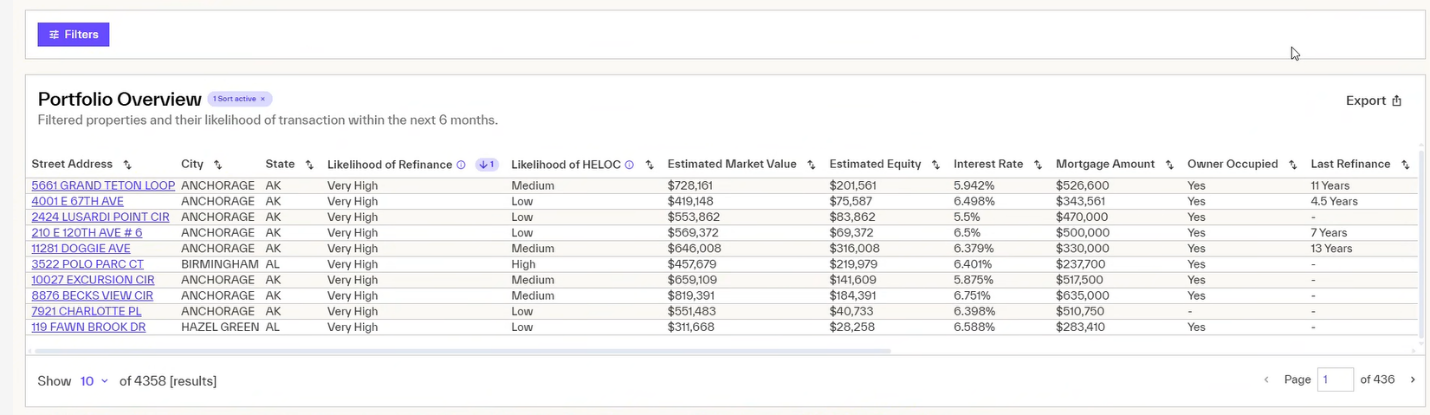

Propensity Intelligence, available through Araya, is a no-code solution that shows the likelihood of a property to HELOC or HELOAN in the next six months.

- See which properties are likely to transact so that you can “see around corners” and build a tailored retention strategy

- No data scientists? No problem. Access the predictive data at your fingertips in an easy-to-understand interface.

Take your “Low Risk” list you curated in Step 3 and create proactive outreach for those customers with a high or very high likelihood to HELOC. Now, you don’t have to guess about who in your book of business is ready for a home equity product.

5. Final validation: Integrated credit data

After the “low risk” population is identified (steps #1, #2, and #3) and for that population those “very high” or “high” in likelihood are selected, one has arrived at a list that is both “low risk” and “high propensity.” Once can now shift the focus from property to borrower. The lender call pull credit data directly within the PIM platform. This allows you to:

- Verify senior liens: Match credit report tradelines to recorded voluntary liens to confirm the exact Unpaid Principal Balance (UPB).

- Assess payment behavior: Review current payment status and amounts to ensure the borrower is managing their existing debt responsibly.

Conclusion

Revenue growth in a tight market isn't a volume game; it's a precision game. By combining PIM’s risk-cleansing capabilities with the Propensity Intelligence predictive power, lenders can stop wasting energy on the "who NOT to contact" and focus exclusively on the borrowers most likely to close.