The high-altitude risk: HOA liens and the evolving landscape in Colorado

Colorado’s "true" super lien environment gives HOAs significant leverage over mortgage lenders. While legislation (HB 22-1137) initially caused a sharp decline in lien volumes due to new regulatory hurdles, recent data shows a significant rebound as compliance stabilizes. For servicers, this signals a critical need for proactive monitoring of HOA-related delinquencies to mitigate risk in a market where small unpaid balances can take priority over first mortgages.

Colorado’s real estate market is defined by its stunning geography, a robust economy, and a heavily sought-after outdoor lifestyle. From the dense, towering condominiums of downtown Denver to the sprawling single-family suburban developments of Colorado Springs and Fort Collins, Homeowner Associations (HOAs) maintain and govern developments and properties housing millions of residents. However, Colorado’s unique legal framework gives HOAs significant leverage over homeowners and mortgage lenders alike in the event HOA fees are not paid.

A true super lien environment

Colorado remains one of the more established “true” super lien states, meaning that a portion of unpaid HOA assessments equal to up to six months of dues can take priority over a first mortgage. For servicers, this introduces a different level of exposure than in states with limited lien frameworks. HOA-related delinquencies can escalate quickly if not addressed, particularly in jurisdictions where enforcement mechanisms are well established.

A market that shifted – then rebalanced

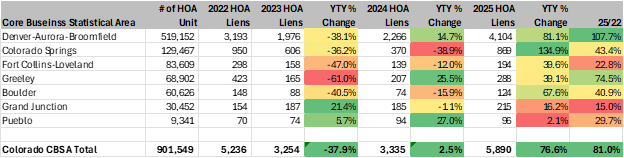

According to recent data tracking of HOA lien volume figures from 2022 through 2025 by Cotality™ and reflected in the chart above, Colorado tells a more nuanced story than a simple upward trend.

In 2022, the Colorado legislature passed HB 22-1137, fundamentally altering HOA collection practices. The bill placed heavy restrictions on an HOA's ability to foreclose. It requires associations to offer mandatory payment plan options prior to proceeding to foreclosure, restricts the amount of fines that can be levied, mandates strict notification procedures (including sending notices in a homeowner's preferred language), and strictly prohibits HOAs from foreclosing solely based on unpaid fines or legal fees (foreclosures must now be strictly based on unpaid regular or special assessments).

Following the passage of HB 22-1137, lien volumes declined sharply across major markets. In the Denver-Aurora-Broomfield CBSA, for example, liens fell by approximately 38% between 2022 and 2023. Similar declines were observed in Colorado Springs (down 36%), Fort Collins-Loveland (down 47%), Greeley (down 61%) and Boulder (down 41%). Rather than signaling a resolution of underlying pressure, this decline could reflect a temporary pause in collection activity as HOAs and management companies adjusted to new regulatory requirements.

More recent projections suggest that activity is beginning to normalize. In Denver, lien volumes are projected by Cotality to reach more than 4,100 in 2025—an increase of roughly 80% from 2024 levels. Colorado Springs shows an even sharper projected increase, with lien activity more than doubling year over year, alongside more moderate increases in other major markets. Taken together, the data suggests a market that contracted under new regulation and is now recalibrating as compliance frameworks stabilize.

What this means for servicers

Colorado’s environment reinforces the importance of visibility into HOA-related obligations as part of a broader servicing strategy. Because of the super lien structure, even relatively small unpaid balances can carry disproportionate risk if left unaddressed. These situations may evolve over a longer timeline, requiring sustained monitoring rather than immediate escalation.

Additionally, the recent rebound in lien activity suggests that what appeared to be a decline in borrower distress could be logically interpreted as a function of delayed collections rather than improved underlying conditions. For portfolios with exposure to Colorado, particularly in high-density HOA markets, this underscores the need for:

- Early identification of HOA-related delinquencies

- Ongoing borrower engagement where additional obligations may be emerging

- A more localized understanding of how regulatory changes are influencing timelines and outcomes

Colorado remains one of the most prominant super lien states in the country, granting HOAs extraordinary leverage to protect their financial interests—even at the expense of primary mortgage lenders. While laws like HB 22-1137 have provided homeowners with temporary relief, recent data suggests a return to more typical patterns as associations adapt to new requirements. At the same time, the state’s super lien framework continues to differentiate it from other markets, introducing unique considerations for servicers and lenders. As these dynamics continue to play out, a more proactive and informed approach to HOA-related exposure will remain essential.