Overview

A powerful winter storm affected the Northeastern United States from Feb. 22 through Feb. 23, bringing blizzard conditions, heavy snowfall, and widespread disruptions across portions of the Interstate 95 corridor. The National Weather Service issued blizzard warnings in parts of the region, including New York City — the city’s first blizzard warning in nearly a decade. Officials warned that travel could become dangerous to nearly impossible in the most heavily impacted areas as strong winds combined with steady snowfall to significantly reduce visibility.

The storm intensified rapidly as it tracked northward along the East Coast, developing into a major coastal low characteristic of a nor’easter. Atmospheric conditions supported rapid strengthening offshore, consistent with explosive cyclogenesis. Forecasts indicated that many communities under blizzard warnings could receive approximately 1 to 2 feet of snow. In the most intense snow bands, snowfall rates approached roughly 2 inches per hour, leading to rapid accumulation and deteriorating road conditions. Wind gusts in exposed and coastal areas were forecast to reach 60 to 70 mph, producing blowing snow and near-whiteout conditions at times.

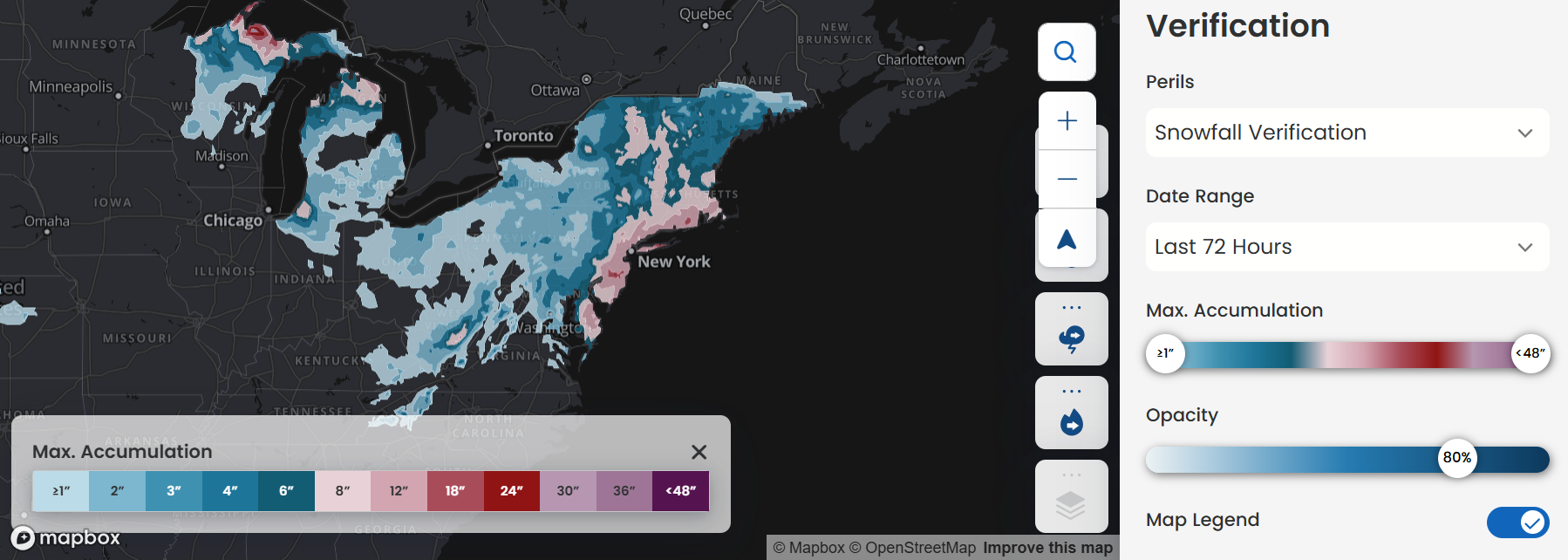

Figure: February 2026 winter storm snowfall accumulation. Source: Cotality Weather Insight (February 23, 2026)

The impact

These dynamics resulted in substantial societal and infrastructure impacts. Hundreds of thousands of customers across the Northeast experienced power outages as heavy snow and wind brought down trees and utility lines. Airlines canceled thousands of flights during the two-day event, disrupting regional and national air traffic. Several states implemented travel restrictions or emergency measures as highways and secondary roads became hazardous due to accumulating snow and drifting. Along portions of the Mid-Atlantic and New England coastline, strong onshore flow increased the risk of coastal flooding during high tide cycles, particularly in vulnerable low-lying areas.

Storms of this magnitude generate a complex loss profile for the insurance sector. Significant winter weather events in the Northeast typically produce insured losses from wind damage, structural stress caused by snow and ice loads, fallen trees, and freezing-related water damage when prolonged outages disable heating systems.

The ultimate financial impact will depend on geographic concentration of losses, policy deductibles, and coverage penetration in coastal and metropolitan areas. When multiple perils — wind, snow load, and coastal water intrusion — occur within a single event, claim adjustment can become more complicated, particularly in distinguishing covered wind-driven damage from excluded flood losses.

Standard homeowners insurance policies generally cover wind damage and damage resulting from the weight of snow or ice. However, standard policies typically exclude flood damage — including storm surge and tidal inundation — requiring separate flood insurance coverage through the National Flood Insurance Program or a private flood policy. Property owners without flood coverage may therefore face uninsured losses if coastal flooding occurred.

Recent increases in construction and rebuilding costs have also heightened concerns about underinsurance. If dwelling limits do not reflect current replacement costs, policyholders may encounter out-of-pocket expenses when repairing structural damage. As adjusters report and process claims in the weeks following the storm, insured and uninsured loss totals will provide greater clarity regarding the event’s overall economic footprint.

"The financial impact of this storm could be significant," notes Tom Larsen, Assistant Vice President of Product Marketing at Cotality. "As the snow melts, we anticipate discovering further 'hidden' losses, such as flooded basements from frozen pipes, that are typical of events this severe. While we expect disruptions to subside as temperatures stabilize, this event serves as a stark reminder of increasing weather volatility. True resilience requires more than just an insurance policy; it requires proactive preparation."

Cotality will continue to monitor this event and provide updates as new information becomes available.