Overview

- Total loan commitments fell 6.2% in the March quarter due to RBA hikes and low confidence.

- Owner-occupiers pulled back faster than investors, pushing the investor share of loan volumes to a record 41.0%.

- First home buyers showed relative volume resilience, though their average loan size fell by 2.6%.

- Continued stretched affordability, renewed rising rates and tighter government tax policies are expected to drag on future investor activity.

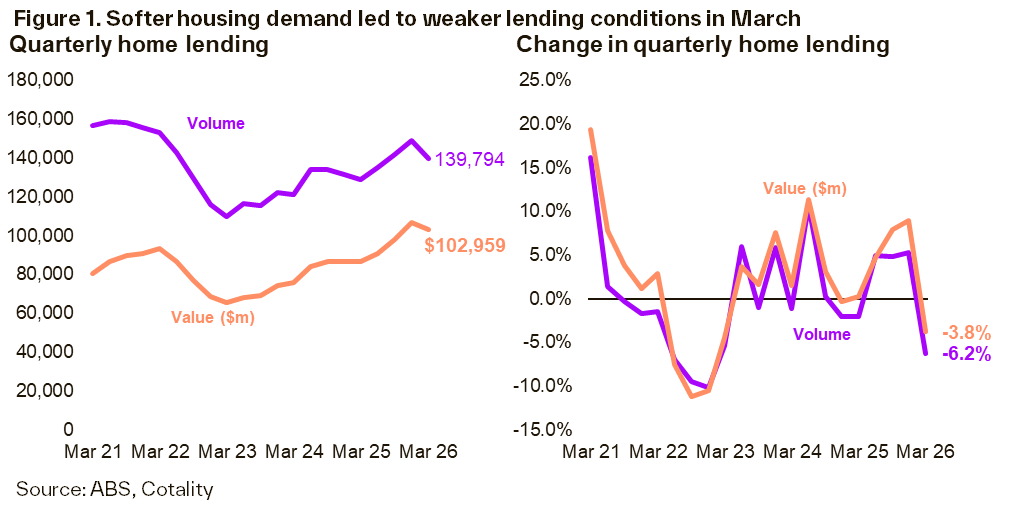

Squeezed by renewed RBA rate hikes and plunging consumer confidence, Australia's housing demand took a measurable hit in the March quarter.

The latest ABS Lending Indicators reflect this shift showing weaker activity than in December last year. The total number of housing loan commitments fell by 6.2%, while the overall value of lending dropped by 3.8%. That said, both measures remained higher than March 2025, reflecting the tailwinds of the solid upswing in lending after last year’s rate cuts.

A number of factors have contributed to the slowdown in housing demand. Measures of housing affordability and mortgage serviceability were already looking stretched last year, even before the Reserve Bank of Australia started lifting interest rates (with two of the three hikes so far this year occurring in the March quarter). Consumer confidence surveys also plunged on the back of rising energy prices as the Iran war commenced in late February, with low confidence often acting as a deterrence to a high value purchase, such as a real estate.

Owner-occupiers led the retreat, but investors not far behind

All categories of property buyers recorded a quarter-on-quarter decline in lending activity, however owner-occupier lending slowed more significantly than investors. The quarterly volume of owner-occupier loans fell by 6.9%, while the volume of investor lending was 5.3% lower. A similar trend was also evident in value terms, with owner-occupiers down by 4.3% versus a 3.0% fall for investors.

This meant that the investor share of total lending rose in March. In volume terms, the investor share was at a record high of 41.0% (albeit this series only goes back to September 2019). In value terms, the investor share was 40.3%, its highest level since December 2016, a period just prior to APRA placing a limit on interest only lending (that was heavily directed towards investors) and two years after APRA had imposed a 10% speed limit on investment lending growth.

Within the owner-occupier space, there was a smaller fall in the volume of lending to first home buyers (FHB) than there was to other owner-occupiers, however this trend was reversed in value terms. This suggests that the average new loan size for FHBs fell in the March quarter, down around 2.6%, compared with a 1.6% increase for other owner-occupiers. In part, this relative resilience in FHB lending may have been supported by the 5% Deposit Scheme.

There was considerable variation in lending trends by state. The overall decline in the volume of investor lending was led by NSW (the state with the largest share of investor lending at 43.9% in March), followed by WA. In contrast, the volume of investor lending in both SA and TAS increased in March, with the volume of investor loans in TAS rising by almost 74% over the same period last year (albeit this increase was off a small base).

The largest decline in first home buyer lending volume was recorded in SA, down by 6.1% in March, while QLD fell by 5.8%. In contrast, TAS eased by 0.7% and WA fell by 2.0%.

Overall, VIC continues to lead FHB lending activity as a share of the total, with Melbourne’s relative affordability advantage over other cities, as well as tax policy settings that discourage investors, contributing to this trend. That said, this share has fallen in recent quarters as the share of investor lending has accelerated. WA has seen a notable pickup in FHB activity as well, while NSW continues to lag.

Where is lending likely to go to from here?

At the national level, the housing market is already on the cusp of a downturn, with dwelling values already contracting in Sydney and Melbourne while growth is slowing in the mid-tier capitals. Demand is likely to soften further, as the full impact of the interest rate tightening (particularly the hike in May) has not yet been felt. There is the possibility that the RBA could continue to lift rates in the short term, given trimmed mean inflation has remained stubbornly above the central bank’s target range.

Compared with other property purchasers, first home buyers tend to be more rate sensitive than others, meaning that we may see a further slowdown in FHB lending activity in coming quarters. This trend would be likely to reverse once the RBA is eventually able to cut interest rates once again, although the impact is likely to remain uneven across the country, influenced by the relative affordability of different markets.

Policy changes in this year’s Federal Budget are likely to have a negative impact on investor demand, and by extension, new investor loans. The removal of negative gearing for purchases of existing properties is likely to reduce investor lending on a net basis; while some new investors may be drawn to purchase newly constructed properties (where negative gearing is retained), they have historically favoured existing dwellings and may now look to other (non-property) assets instead. With rental yields well below the cost of borrowing (particularly if interest rates rise further), fewer investors into existing properties would be able to generate a positive cashflow, meaning that the costs of holding these assets are now substantially higher and serviceability challenges more prominent.