Overview

- While the national market remains well-balanced, a deeper dive into population and dwelling data reveals that the supply of new homes in major cities like Wellington and Auckland has outpaced population growth, leading to a loosening of market conditions.

- This trend stands in contrast to other parts of the country where a tightening of supply is still putting a bit of pressure on the housing market.

Analysis from Kelvin Davidson, Cotality NZ Chief Property Economist

New analysis from Cotality shows a significant shift in the balance of property supply and demand across New Zealand, with key regions experiencing a notable easing.

While the national market remains well-balanced, a deeper dive into population and dwelling data reveals that the supply of new homes in major cities like Wellington and Auckland has outpaced population growth, leading to a loosening of market conditions.

This trend stands in contrast to other parts of the country where a tightening of supply is still putting a bit of pressure on the housing market.

Strong supply growth in Auckland & Wellington

Based on the analysis, Wellington and Auckland are two primary areas in New Zealand where property supply has outpaced population growth between 2019 and 2024.

In Wellington, the population actually saw a small decline of 1.0% in the five years to 2024, while the dwelling stock increased by 4.3%. This caused the occupancy rate to drop from 2.97 to 2.82. While the recent property value downturn is partly an unwinding of previous affordability stress, this loosening of the supply and demand balance also played a role.

Auckland's population grew by a robust 7.0% over the same period, but this was exceeded by an even stronger 10.3% increase in dwelling stock. This eased Auckland's occupancy rate from 3.45 to 3.34.

This easing in the physical supply and demand balance aligns with the weakness in Auckland's property values, although it is also worth noting that the recent construction mix in Auckland has been dominated by townhouses, which are smaller and have a naturally lower occupancy rate.

Conversely, areas like Hamilton and Tauranga are seeing a tightening of the supply/demand balance, as their population growth has outpaced dwelling supply – more detail on the next page.

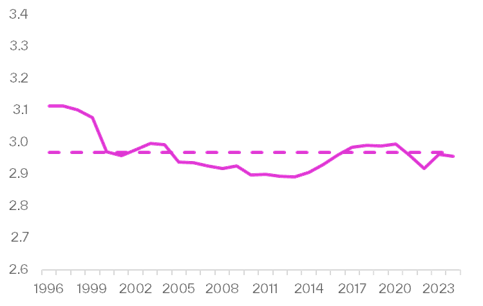

Nationally, from 2019 to 2024, the population grew by 6.4%, while housing stock increased by 7.5%. This resulted in the average number of people per dwelling, or occupancy rate, easing from 2.99 to 2.96 over the five-year period. This figure suggests that the overall market is well-balanced, with the long-run average of 2.97 people per house sitting close to the current rate. This balance is also supported by the recent lack of growth in property values and rentals.

Chart 1: NZ people per dwelling

Chart 2: NZ annual % change population and dwellings

A varying picture across other areas

Other main centres, such as Tauranga and Hamilton, present the opposite scenario, with double-digit population growth outpacing the rise in dwelling stock. Between 2019 and 2024, Hamilton's population increased by 10.3% while its dwellings grew by 8.1%, and Tauranga saw population growth of 10.2% compared to a 5.9% rise in dwellings. Although these areas are not experiencing a property value boom, their markets have been more resilient than those in Auckland and Wellington, with less improvement in housing affordability.

Focusing on other population hotspots, like Selwyn, Queenstown-Lakes, Waikato District, and Waimakariri, construction activity has largely kept pace with population growth. From 2019 to 2024, dwelling stock grew by 12.7% in Waimakariri, 29.8% in Selwyn, and 13.8% in Waikato. Market feedback suggests these areas are well-balanced in terms of property availability and do not show the same clear affordability strains.

However, Queenstown-Lakes remains an exception. Despite its dwelling stock growing slightly faster than its population between 2019 and 2024, the area's property values remain high and affordability pressures intense. This highlights the unique market dynamics of Queenstown, where accumulated wealth helps to insulate property values even with strong supply growth.

Supply and demand isn’t everything, but still vital

While the physical supply and demand balance over short periods does not explain all changes in property values or affordability, it is obviously an important factor. Other influences, such as available listings, or changes in wealth and income, also play a significant role. However, when looking at this data in isolation, it suggests that property values in Wellington and Auckland may remain relatively soft, while other main centres like Hamilton and Tauranga could see stronger performance.

Chart 3: % change in populationand dwellings 2019-24