Overview

- This Pulse article looks at the latest Buyer Classification figures to explore the comeback by mortgaged multiple property owners.

- Their market share has risen across many parts of the country, led by ‘Mum and Dad’ buyers – who are enjoying lower mortgage rates and reduced top-ups on rental properties.

- Investors also appear to be securing sharper deals, paying a lower median price this year than in 2024.

Overall buyer trends remain consistent

Many of the longer-term patterns in Cotality’s Buyer Classification data have continued in recent months. Relocating owner-occupiers (‘movers’) remain more cautious than usual, while first home buyers (FHBs) are still active at elevated levels. Mortgaged multiple property owners (MPOs) are also making a steady comeback.

This Pulse focuses on mortgaged MPOs – including investors – who have been returning to the market over the past year, encouraged by several regulatory changes including the shorter Brightline Test, reduced deposit/LVR requirements (from mid-2024), and the full reinstatement of mortgage interest deductibility from 1 April 2025.

Lower mortgage rates have added further support, reducing the cashflow top-ups out of other income that are typically needed for investment purchases.

What are mortgaged MPOs buying and paying?

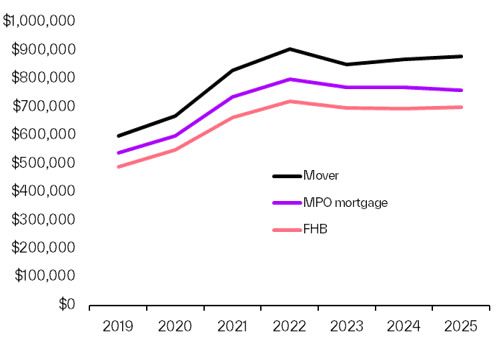

So far in 2025, mortgaged MPOs nationally have paid a median of $759,000, slightly down from $770,000 in 2024. That’s higher than the $700,000 median first home buyers have paid (up from $695,000 last year). Movers have paid $880,000 this year compared to $870,000 in 2024.

The small dip in the MPOs’ median price isn’t because they’ve shifted to cheaper properties. In fact, their share of standalone house purchases has edged up from 66% last year to 67% in 2025, still below FHBs and movers, where standalone dwellings account for 75% of activity each for the same period.

New builds remain a significant part of mortgaged MPO activity. This year, they account for around 30% of the new-build market, only marginally lower than 31% in 2024 but still well above the 25% share in 2020, before Labour’s property tax changes.

New-builds continue to appeal because they’re exempt from LVR and DTI restrictions, even though some earlier tax benefits have gone. The trade-off for investors is that new-builds generally come with higher purchase prices and less scope to create gains through renovation.

Chart 1: NZ% share of property purchases per quarter

Chart 2: Median price paid by different buyer groups

A broad-based upturn in demand

The share of purchases by mortgaged MPOs has lifted from cyclical lows of around 22% in 2022–24 to nearly 24% in 2025. While first home buyers still dominate in Wellington, investor activity has strengthened across the other main centres over the past 12–18 months, reaching close to 29% in Hamilton, 27% in Christchurch, and 26% in Auckland. Tauranga and Dunedin have also recorded higher investor presence.

A similar trend is evident outside the main centres. In Gisborne, MPOs’ share of property purchases has jumped to 30% this year from 23% in 2024, while Invercargill has risen from 20% to 27%. Rotorua also has a higher share than the national average at 28% alongside Hastings which has climbed to 25% from 21% in 2024.

The return of ‘Mums and Dads’

Analysing the data by portfolio size shows the recent increase in MPO activity has come entirely from smaller players, either new investors who own two properties (e.g. their home and one investment) or those with a small portfolio already, of up to three investment properties.

There’s no set definition of a ‘Mum and Dad’ investor, but the data suggests that the smaller buyers are driving wider activity. With potential top-up costs falling many appear to be using equity in their own home or across their existing portfolio of rental dwellings to step into the market.

Table 1: Mortgaged MPOs’ % shareof property purchases