Overview

- A record number of existing mortgage holders changed lenders in June, likely reflecting the short-term structure of many loans and the current ability to switch with minimal or no break fees.

- While other lending trends remained in place, this rise in refinancing remains a continued focus for the banks and shows that mortgage holders are actively monitoring rates and terms as conditions shift.

- With a high share of borrowers coming off fixed terms over the next six months or so, it’s possible this switching behaviour may remain elevated for a while yet.

Analysis from Kelvin Davidson, , Cotality NZ Chief Property Economist

A record number of existing mortgage holders changed lenders in June, likely reflecting the short-term structure of many loans and the current ability to switch with minimal or no break fees. The cashbacks being offered are the incentive to take advantage of these conditions.

While other lending trends remained in place, this rise in refinancing remains a continued focus for the banks and shows that mortgage holders are actively monitoring rates and terms as conditions shift. With a high share of borrowers coming off fixed terms over the next six months or so, it’s possible this switching behaviour may remain elevated for a while yet.

The latest Reserve Bank figures showed $8.3bn of new mortgage lending activity in June, which covers house purchases, loan top-ups (also known as equity withdrawal), and bank switches, often referred to as refi(-nancing). That was a $2.6bn increase on the same month last year, although it should be noted that June 2024 was a ‘one off’ soft month.

Both investors and owner-occupiers remain part of the upswing, and more specifically so too do first home buyers (FHBs) – that’s fully consistent with the Cotality Buyer Classification figures.

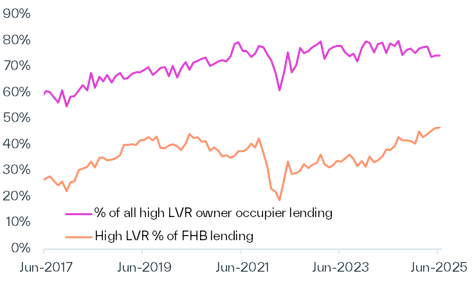

Meanwhile, across all owner-occupiers, the loan to value ratio limits are still not really being tested – 12.1% of lending in June was done with a deposit less than 20% – but this type of lending remains popular with FHBs. They still account for 75-80% of all low-deposit owner-occupier activity, and nearly half of all FHBs are entering with less than a 20% deposit (or loan-to-value-ratio, LVR, of greater than 80%).

Around 15% of owner-occupiers (by value) took out interest-only debt in June, and almost 35% of investors. Going back to 2017, those figures were closer to 30% and 50% respectively, so interest-only lending could be considered ‘under control’ at present. Interest-only lending remains well below past peaks, with no strong indication it is being used to manage financial stress, as was observed during COVID.

Chart 1: FHB lending at high LVR (>80%)

High DTI lending is drifting upwards but well short of speed limit

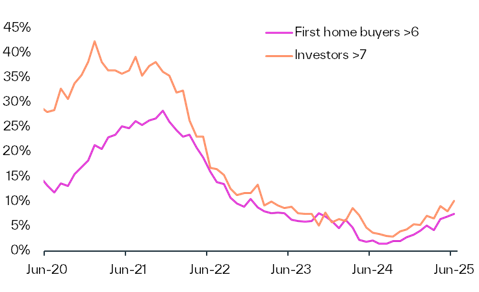

The upward drift for high debt-to-income (DTI) lending continued in June as the internal serviceability test rates at the banks ease. For investors, 10.2% of loans by value were done at a DTI greater than 7, the highest share since 13.5% in January 2023. Among first home buyers, 7.5% of loans went out at a DTI above 6, the highest share since October 2023.

While still well below the 20% regulatory speed limits, these figures show that high DTI lending is gradually becoming more common again. That said, with house prices relatively flat, many borrowers don’t need to stretch as far to secure finance. Even so, the DTI framework remains a key constraint in the background, especially for investors looking to quickly expand their property portfolio.

Chart 2: % of lending at high DTI

Refinancing activity reaches record high

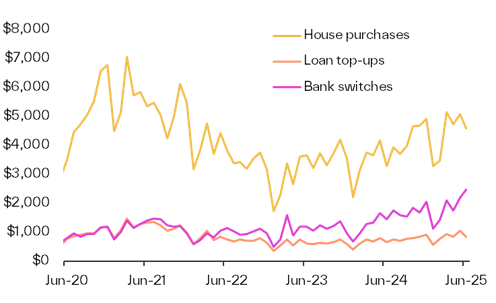

Perhaps the most striking aspect of the June lending data was the level of refinancing. More than 3,500 existing mortgage holders switched banks, accounting for nearly $2.5bn in lending - both comfortably record highs for this data series going back to 2017.

This elevated level of switching likely reflects a mix of factors, including the increasing role of mortgage advisors, rising consumer awareness of lending options, and the continued level of cashbacks being offered.

Just as significant is the structure of loans. With nearly 14% of mortgages on floating rates and another 39% fixed and due to roll off by the end of 2025, a large number of borrowers are in a position to switch lenders without large break fees. This dynamic may continue to support elevated levels of refinancing activity in the near term.

Chart 3: Value of lending ($m)

Refinancing may influence activity ahead

It’s often difficult to determine whether improved credit conditions are driving more property transactions, or whether rising sales volumes are simply generating more lending activity. In reality, it’s probably a combination of both. What is clear is that sales activity has broadly returned to more typical levels, and this is starting to weigh on listings with the volume of stock on the market edging lower, helped by the likelihood that some vendors are actively withdrawing their properties too.

That stabilisation could lead to more competitive price pressures in the coming months. However, with economic conditions still subdued and job security lower than in previous cycles, any lift in values is likely to remain modest. Following a 0.6% rise in national median values in the first half of 2025, a further 1-2% increase across the second half of the year appears to be a reasonable expectation.

One final factor worth monitoring is how existing borrowers respond as their interest rates continue to fall. The average fixed mortgage rate currently being paid is around 5.8%, while market rates are typically now below 5%. As loans mature, borrowers will need to decide not only what term to refix on, but also what to do with their ‘cash windfall’ from lower repayments. Some may use that capacity to reduce the length of their mortgage (by keeping repayments the same), while others may save it, thereby reducing the pass-through to economic activity.

It's also worth noting there is a small group of borrowers still sitting on low five-year fixed rates of around 3% that were set during the mid-2021 trough. While they’ll eventually face higher repayments, the benefits they’ve already seen have been significant in the past few years.